Bitcoin Is Good, by Coinbase Founder Fred Ehrsam | Re/code

Jay Liew stashed this in bitcoin

The Coinbase founder Fred Ehrsam does not know what he does not know:

We read with interest Paul Krugman’s recent article in the New York Times, humorously titled “Bitcoin Is Evil.” Perhaps the most important part of the article is where Dr. Krugman remarks:

“… when I try to get them to explain to me why BitCoin is a reliable store of value, they always seem to come back with explanations about how it’s a terrific medium of exchange. Even if I buy this (which I don’t, entirely), it doesn’t solve my problem. And I haven’t been able to get my correspondents to recognize that these are different questions.”

Approaching bitcoin as a currency or store of value is focusing on a single and secondary application of the bitcoin network (analogous to analyzing a single feature built on top of the Internet, like email). The first application of the network which has gained broad adoption is payments, where it can be easily demonstrated that real money is being saved by harnessing the efficiency of the network. Since one must acquire bitcoin to use the bitcoin network, this has given bitcoin as a currency value as a secondary effect.

Krugman states that bitcoin does not act as a good store of value because it does not have some kind of inherent floor to its value. Looking at other examples, he implies, gold has decorative and commercial applications and fiat currencies have the backing of their respective sovereign entities. In contrast, bitcoin as a currency has no value unless people use the bitcoin network. If this lack of a clear floor is part of the strict economic definition of a “store of value,” Krugman may very well be correct that bitcoin is not one, but that does not mean the value is not real, nor does it mean that value is ephemeral.

Yes it does mean that the value is ephemeral. That's exactly what it means.

This is a flawed argument:

Going back to Krugman’s acid test for store of value, there is no “floor” to the value of the bits traveling over the Internet, because people could stop using it at any time. However, the Internet will continue to be valuable so long as it is the most efficient mechanism for transferring data. Bitcoin’s value is the same: It will remain as long as it is the most efficient mechanism for transferring ownership.

The Internet is not the most efficient mechanism for transferring data.

Its value has built up slowly over time, and is not subject to wild swings in value.

He says that Bitcoin is more than just a payment system:

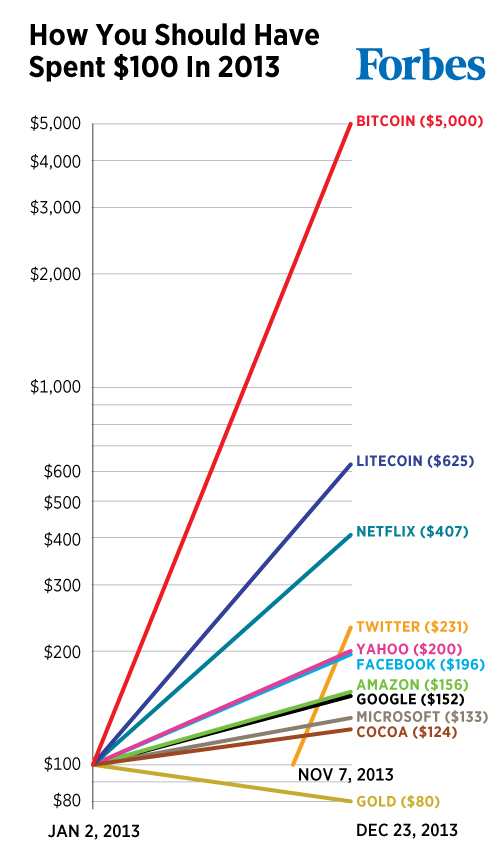

In the present, the value of bitcoin as a currency can be viewed as the sum of the cost savings of using the bitcoin network for payments rather than alternative payment networks. If 1.00 bitcoin is currently used for 10 transactions a year with an average value of $100, the bitcoin network is three percent cheaper than the average next best alternative, and this dynamic is maintained for 10 years, multiplying these arbitrary sample inputs values 1.00 bitcoin at $300. This does not require bitcoin to replace existing local currencies.

Again, bitcoin as a payment system is just one of the potential applications of the network. To cap bitcoin’s value here would be like saying that the Internet, in the early days, was only as valuable as its ability to send email in a more efficient way than fax or snail mail. Bitcoin is valuable as a currency because of the economic efficiencies the bitcoin network is already creating as transactions flow over it. As with the Internet, more applications will flourish which will make the bitcoin network, and thus bitcoin as a currency, valuable.

But there can be no efficient transactions with Bitcoin while Bitcoins themselves have wild price volatility.

Coinbase attempts to legitimize itself by drawing comparisons to eBay and Airbnb:

We are content leaving the question of traditional and strict definitional “store of value” to economists better educated in their field than ourselves. That said, we are sufficiently convinced in the value of the bitcoin network. It is delivering tangible economic value first and foremost as a payment system in the present. This will continue to evolve in the future in ways we can foresee now — for example, securities clearing in a distributed, paperless and trustless manner — and in future applications we cannot, in the same way no one foresaw eBay or Airbnb in the early days of the Internet. This is the power and excitement of technological advancement at a low (in this case, protocol) level. It allows things to be built — and thus long-term value to be created — in ways which were not previously possible.

eBay and Airbnb are TRUSTED NETWORKS with fraud prevention assurances.

I see no such assurances by anything dealing in Bitcoin.

Adam, I agree with most of your points, but this one I have learned a slightly different perspective on after immersing myself in the Bitcoin space over the past few months.

Bitcoin has an entirely different approach to trust, and ironically, it is "Trust no one". In practice, this means that every transaction is verified by multiple, independent 3rd parties, so that no single entity can violate the system. Trust comes from verification.

Normally the banks/payment processors are there to play this moderator (arbiter) role. The idea behind bitcoin is to cut out the middleman, and have The Internet verify the transaction. Bitcoin is bittorent-for-money. No single point of failure.

For more info, I highly recommend reading the bitcoin whitepaper http://bitcoin.org/bitcoin.pdf

As for Bitcoin being a viable currency for the Internet to replace old world currencies, I see two big hurdles.

1) Currency vs Commodity. Since bitcoin was modeled after Gold (finite supply, miners show proof-of-work), it is deflationary, and attracts speculators. The current price fluctuations make it unsuitable for business transactions. Can you imagine trying to run an online e-commerce shop with your prices in BTC? By the time your shopper gets to the end of the checkout process, the price could have swung 15%. We need more stability.

2) Chargebacks. Bitcoin transactions are not reversible. As a consumer, I take comfort in using my Visa/MC, knowing that they have my back and will reverse the charge if I run into problems using it. For the record, I've never had to use it, but I know that I could if I had to. This comfort enables me to make purchases with Strangers. The bitcoin protocol has the concept of multiple party transactions, which I believe could be used to create an escrow system where 2 of the 3 parties have to agree before the funds are released. But it's a bit complex, and there are no consumer-friendly implementations yet.

It remains to be seen if Bitcoin will be able to solve these problems or if it will be Bitcoin's replacement that comes along and does it. But make no mistake, the stage is being set for the biggest old-world-vs-new-tech war we have ever seen. Print vs New Media, RIAA vs MP3, Hollywood vs Bittorent... those will all look like cat fights compared to the battle between Old Money vs Digital Currencies.

Thanks, Nick, that whitepaper is excellent.

So it's not the protocol itself, but the implementations, that allow thieves to pilfer Bitcoins?

I don't think Fred Ehrsam does himself any favors when he calls Paul Krugman hilarious.

That flip attitude reminds me of the Rap Genius founders:

http://pandawhale.com/post/34660/rap-genius-founders-are-jean-ralphio-gifs

Good stuff. Thanks for sharing, Adam! Appreciate your input. Definitely lots of people for and against BTC, and like anything else, it's easy for comments online to include personal feelings and degenerate from there, instead of sticking to the facts. Time will tell how this plays out!

That's true.

It's still hard for me to see Bitcoin as more than a zero-sum game.

Which means: Every time someone profits it's because someone else put money in that s/he will eventually lose.

Am I wrong?

http://pandawhale.com/post/32804/bitcoins-the-second-biggest-ponzi-scheme-in-history

11:24 AM Jan 03 2014