How much can I save with a student loan refinance?

Adam Rifkin stashed this in Student Loans

Stashed in: Personal Finance

The nerdwallet link has a table with how much the average savings for a refinance would be.

Refinance savings average between $3000 and $13,000.

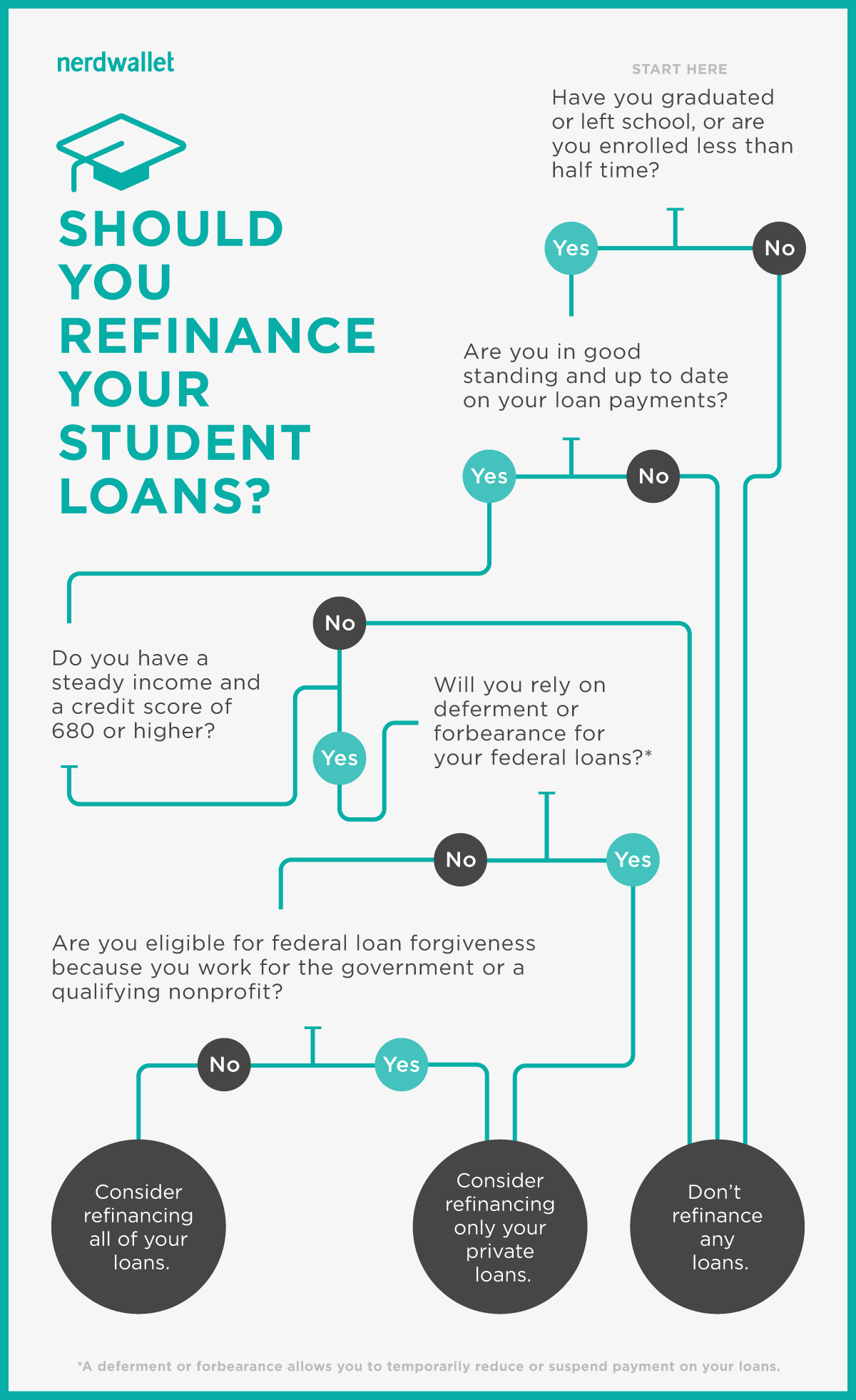

Nerdwallet on Should I Refinance:

Refinancing might not be in your best interest, even if you qualify. If you refinance your federal loans into a single private loan, you risk losing certain advantages, such as flexible repayment plans, public service loan forgiveness and interest-free deferment on subsidized federal loans if you lose your job. It’s important to research all student loan repayment options before you decide to refinance.

You should consider refinancing your student loans if the following are true:

- You have a good credit score. Refinancing companies consider grads with scores in the 690s or above to be the most reliable. If you have a lower score, you might be denied or your refinance options might not offer a better rate.

- You have a steady income and job security. Lenders want to make sure you can pay them back. A full-time job makes you a more reliable candidate to make monthly payments on time and in full.

- You’ve made steady payments for at least two years. Desirable refinancing candidates demonstrate a positive track record of consistently repaying their loans on time and in full each month. If you’ve done that for at least a couple of years, you’re seen as less risky.

- Most of your loans are private. You’ll save more by refinancing private debt because the average annual percentage rate on these loans is typically much higher than the APR on federal loans.

- You have high debt. Refinancing is most beneficial if you have high debt. You need to have at least $7,500 in total loans to consider the option.

Here's a few examples:

Scenario 1 – Simple refinance

Assume a $15,000 balance at 6.8% with a refinance offer at 3.5%.

See the math above? Although a savings of $25 a month may not seem significant, it is. When your student loans are all done, you’ll have saved $2,800 in interest – that’s more than a 50% decrease in interest paid. This is a refinance scenario that’s worth your while.

Scenario 2 – Multiple Loans

Assume three loans: $15,000 at 6.8%, $10,000 at 7.5% and $5,000 at 3.86%, and a refinance offer at 4.2%.

The debt scenarios are endless, but are relatively simple to figure out for yourself. You can use a basic student loan calculator to see what the ultimate cost of your current student loans is and then based on your refinance percentage offered, run the calculations again at the new rate. This will allow you to see which loans are advantageous for the refinance and to identify those that you may or may not want to wrap up in the new loan.

Source:

https://www.tuition.io/blog/2014/02/how-much-can-you-save-if-you-refinance-your-student-loans/

Consolidating loans can help:

http://www.bankrate.com/finance/college-finance/faqs-on-student-loan-consolidation-1.aspx

Student Loan financial aid flowchart:

https://www.estudentloan.com/resources/student-loan-graphics/financial-aid-flowchart

1:55 PM Feb 25 2016